The Chief Audit Executive (CAE) holds a critical leadership role within an organization, overseeing the internal audit function. Reporting directly to senior management and the board, the CAE ensures that the organization’s internal controls, risk management processes, and governance practices are operating effectively. Here’s an overview of the CAE’s key roles and responsibilities when it comes to auditing:

1. Strategic Leadership of the Audit Function

As the head of the internal audit department, the CAE is responsible for developing and executing the organization’s audit strategy. This includes:

- Audit Planning: Designing a risk-based audit plan that focuses on areas of the business that are most susceptible to financial, operational, or regulatory risks.

- Resource Allocation: Ensuring the audit team has the necessary skills and tools to effectively carry out the audit process.

Alignment with Organizational Goals: The CAE aligns the audit strategy with the company’s broader business objectives, ensuring that audits focus on areas of strategic importance.

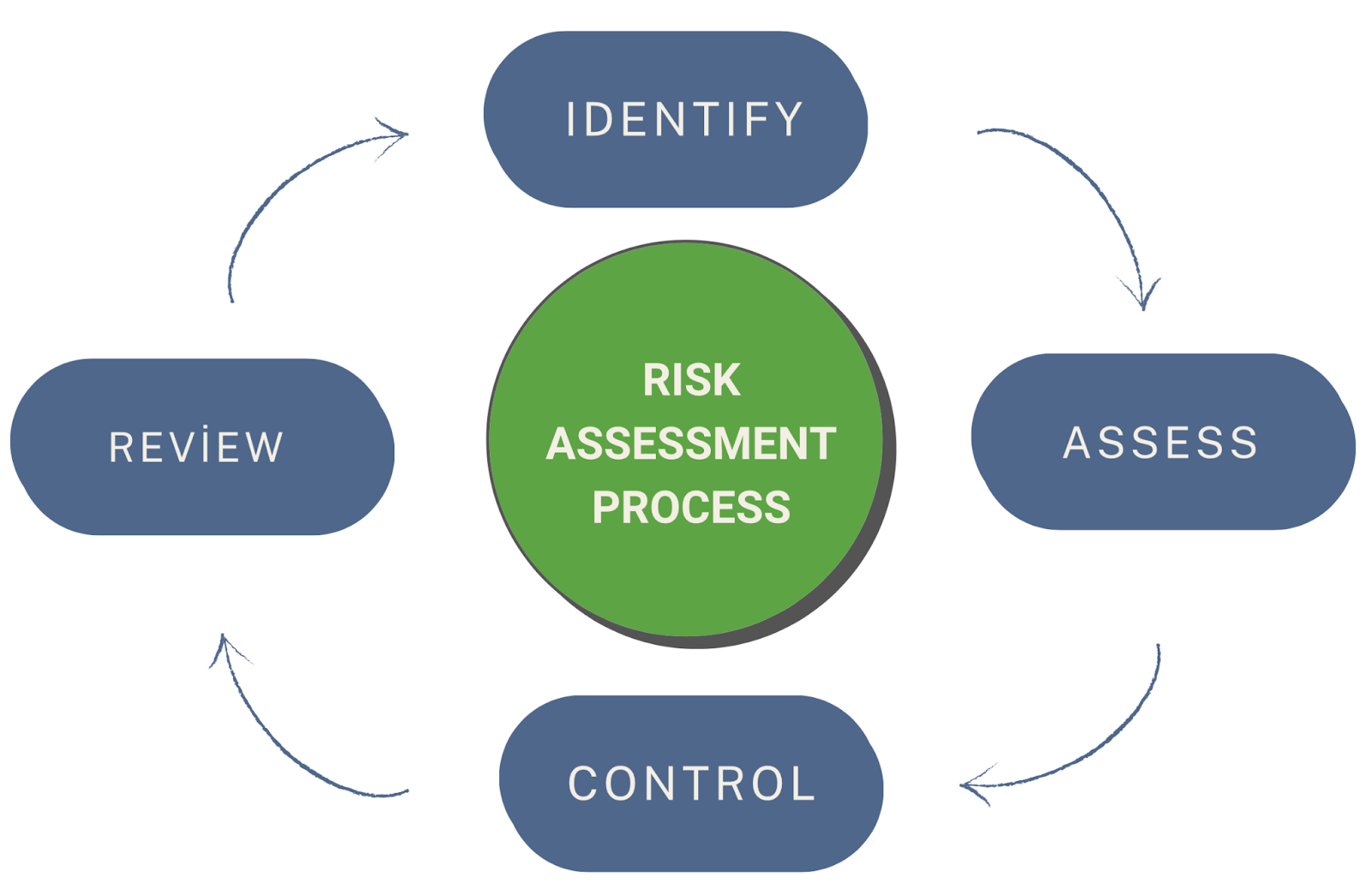

2. Risk Management and Internal Control Assessment

One of the primary functions of the CAE is to evaluate and enhance the organization’s risk management framework. This involves:

- Risk Identification and Assessment: Collaborating with management to identify potential risks to the organization, including financial, operational, and compliance risks.

- Internal Controls: Evaluating the effectiveness of internal controls, recommending improvements to strengthen these controls, and ensuring they align with best practices and regulatory requirements.

By providing assurance that risks are being properly managed, the CAE plays a crucial role in safeguarding the organization’s assets and reputation.

3. Reporting to the Audit Committee

The CAE regularly communicates with the audit committee, which is typically a subset of the board of directors. Key responsibilities in this area include:

- Audit Findings: Reporting the results of audits, including identified risks, control weaknesses, and recommendations for improvement.

- Follow-Up: Ensuring that corrective actions are implemented and monitoring their effectiveness.

- Independence and Objectivity: The CAE must maintain independence from operational management to ensure unbiased reporting, which is critical for effective governance.

4. Ensuring Regulatory Compliance

The CAE ensures that the organization adheres to applicable laws, regulations, and standards, such as the Sarbanes-Oxley Act (SOX) and the International Financial Reporting Standards (IFRS). This includes:

- Compliance Audits: Conducting regular audits to assess compliance with regulatory requirements.

Policy Enforcement: Ensuring that internal policies and procedures are being followed across departments.

5. Continuous Improvement and Advisory Role

Beyond traditional auditing, the CAE acts as an advisor to management, recommending improvements in areas like:

- Operational Efficiency: Suggesting process improvements to optimize business performance.

Technology and Innovation: Identifying opportunities for leveraging technology to enhance audit procedures and controls.

Conclusion

The CAE plays a pivotal role in maintaining the integrity of an organization’s internal controls, risk management processes, and governance framework. Through strategic leadership, risk assessment, and compliance oversight, the CAE ensures that the internal audit function not only protects the organization but also contributes to its long-term success.